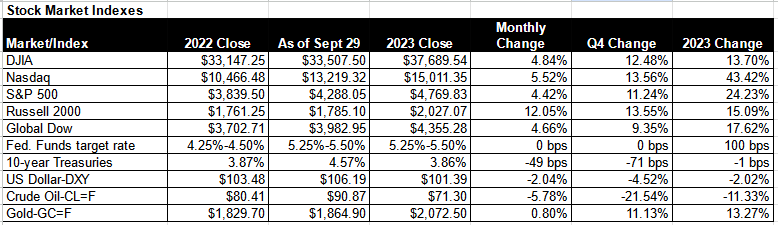

2023: It may be over and as they say, “It’s a wrap!” but it was full of surprises! It was a year that most prognosticators could not have been more wrong about. After an expectation of a moderate year, the market came roaring back in the last quarter with the S&P finishing up 24%, just shy of the January 2022 record. To be honest, that is a bit skewed because the “Magnificent Seven” (the top seven stocks of the index) drove the lion’s share of the S&P 500 Index return. The NASDAQ was up a whopping 43% while the Dow Jones Industrial Average was up only 14% – but who could be unhappy about that?!

The Fed continued to walk the tightrope wire it started on in 2022 to tame inflation without inflicting a recession. They raised rates at a clip not seen since the 1980’s. As interest rates rose, the ever hopeful consumer kept spending and unemployment fell to the lowest level in 50 years to 3.4%. After many years of near zero cash interest rates, CDs, Treasury Notes and money markets peaked at over 5%!

While inflation has turned lower, it remained above the Fed's 2% target. The progress in moderating price pressures allowed the Fed to refrain from further interest rate hikes since July. In addition, and this is important, recent Fed projections indicate rate cuts of three quarters of a percent in 2024, possibly in the form of three 25 basis point rate reductions. Of course, changes in the economy or inflation could prompt the Fed to alter its course of action.

Raising interest rates may have helped drive down inflation, but it also had the most unfortunate effect of cooling the housing market. Rising interest rates also carried over to mortgage rates, which vaulted higher, peaking at about 8% in October, more than double the mortgage rate during the pandemic and well above pre-pandemic levels. Higher mortgage rates translated to fewer buyers however, and home prices climbed higher year over year, primarily due to diminishing inventory. Fortunately, mortgage rates have fallen by more than a full point over the last few months of the year, settling at about 6.61% at the end of December.

In mid-January, the United States hit its debt ceiling, which prompted a political back-and-forth until the beginning of June, when an agreement was reached. The result was new legislation, the Fiscal Responsibility Act of 2023, which effectively raised the debt ceiling but capped federal government spending. We’ll have to wait to see how that works out.

Still, the U.S. economy proved to be resilient in 2023. Gross domestic product expanded during each of the first three quarters of the year, increasing 2.2% in the first quarter, 2.1% in the second quarter, and 4.9% in the third quarter. Consumer spending, the linchpin of the economy, also showed strength, climbing 3.1% in the third quarter. Consumers spent on both goods and services throughout the year.

One of the primary factors in the drop in overall inflation was a decline in energy prices. According to the Consumer Price Index, energy prices fell 5.4% over the 12 months ended in November (latest CPI data available). Gasoline prices dropped 8.9% over the same period. Food prices, on the other hand, rose 2.9%, while prices for shelter increased 6.5%.

As 2023 drew to a close, there were some positives to consider upon entering the new year. The GDP expanded at a greater-than-expected pace in the third quarter, and crude oil and gas prices reversed course and dipped lower. If interest rates decrease, borrowing will be available to more consumers, which should help the housing sector. Let’s hope so.

Stocks enjoyed a solid bounce back in 2023. If corporate earnings continue to rebound, that would bode well for stocks in 2024. There are other factors that will come into play next year, but how they impact the economy and markets is open to speculation. How much longer will the Russia/Ukraine war last, and how much more financial aid will be coming from the United States? The Hamas/Israel conflict could expand to include other countries, impacting other lives and economies. And, of course, 2024 brings with it a presidential election we are unlikely soon to forget.

The chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Snapshot 2023

The Markets

Equities: Stocks began 2023 on a positive note and ended the year trending higher. However, the ride for investors throughout the year was not always a smooth one. Nevertheless, the economy proved resilient, corporate profits rose, and the once anticipated economic recession never materialized. Technology stocks rebounded in 2023, with megacaps and artificial intelligence shares leading the charge. Communication services and information technology gained over 55% and trending notably higher were consumer discretionary and industrials. Utilities, consumer staples, energy, and health care closed lower, however.

Bonds: For much of 2023, bond prices declined, sending yields higher. The yield on 10-year Treasuries reached a high in October at about 4.9% but steadily fell throughout the remainder of the year, ultimately settling right about where they began the year.

Oil: West Texas Intermediate (WTI) crude oil prices began the year at about $80 per barrel then rode a wave of volatility throughout the year, peaking at about $93.68 in late September. Since that time, crude oil prices have steadily declined despite production cuts by OPEC+ and the Israel/Hamas conflict. Decreasing demand and booming oil production by the United States and other oil-producing countries have driven prices lower.

Gold: Gold prices began the year at about $1,830 per ounce and hit a record high of $2,152.30 near the end of 2023. While gold prices began the year on an upswing, that quickly changed. The price of gold retreated as the economy, the dollar, and Treasury yields all saw gains, driving gold prices to a low of $1,809.87 in late February. Then, the financial uncertainty caused by the bank crisis in March and April helped drive up the price of gold to over $2,000 per ounce. Beginning in September, particularly after the Federal Reserve announced that it would hold interest rates steady, interest in gold waned. As prices headed to below $1,800 per ounce, the attacks by Hamas in early October started a war with Israel, sending gold prices past the $2,000 per ounce mark at the end of the year.

Eye on the Year Ahead

Though the crystal ball is still a bit cloudy, these are the things we’ll be keeping a sharp eye on. Will waning inflation and slowing job growth prompt the Federal Reserve to lower interest rates in 2024? And if interest rates are decreased, what impact will that have on the bond and stock market? Will corporate earnings sustain the current market values? Crude oil prices and retail gas prices declined in 2023, but the ongoing conflict in the Middle East, coupled with a cut in production, could force prices for both commodities higher this year. It may well be time to move cash off the sidelines to lock in some higher rates.

At this point, there is much uncertainty surrounding the 2024 election in November. No question, it will hog the headlines. With the field shaping up, chatter about next year’s election is also heating up. Of course, it could impact the economy in general, but, historically, there has been very little difference in stock market returns regardless of which party is in power. In fact, since 1925, US markets climbed 83.3% of presidential election years, averaging 11.4%. Anyway, it’s much too early to give significant thought to the potential market impact.

“This time, like all times, is a very good one, if we but know what to do with it.” – Ralph Waldo Emerson

We wish you all a very Happy New Year and many blessings in 2024. Don’t hesitate to call with any questions or concerns. That’s what we’re here for and walking with you through this financial journey is what we strive to do best.

Your Financial Focus Team

Data sources: Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful. The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The S&P 500 is a market-cap weighted index composed of the common stocks of 500 largest, publicly traded companies in leading industries of the U.S. economy. The NASDAQ Composite Index is a market-value weighted index of all common stocks listed on the NASDAQ stock exchange. The Russell 2000 is a market-cap weighted index composed of 2,000 U.S. small-cap common stocks. The Global Dow is an equally weighted index of 150 widely traded blue-chip common stocks worldwide. The U.S. Dollar Index is a geometrically weighted index of the value of the U.S. dollar relative to six foreign currencies. Market indexes listed are unmanaged and are not available for direct investment. Global Financial Data Inc. as of 7/18/2023, S&P 500 total return, frequency of positivity and acreage return in presidential election years.